Goodwill on financial statements is a critical concept that often perplexes investors, accountants, and business owners alike. It represents an intangible asset that arises when one company acquires another for a price greater than the fair value of its identifiable net assets. Goodwill can significantly impact a company's financial health and valuation, making it essential to comprehend its implications. In this guide, we will delve into the intricacies of goodwill, its calculation, and its impact on financial statements.

When companies undergo mergers and acquisitions, the concept of goodwill becomes particularly relevant. It embodies the value of a company's brand, customer relationships, employee morale, and other intangible factors that contribute to its profitability. Understanding how goodwill is reflected on financial statements can provide valuable insights into a company's performance and potential for future growth. As we explore this topic, we will address common questions and concerns regarding goodwill in financial reporting.

With an increasing number of businesses engaging in acquisitions, the significance of goodwill on financial statements cannot be overstated. Investors and stakeholders must be equipped with the knowledge to interpret these figures effectively. This article aims to demystify the concept of goodwill and its role in financial reporting, ensuring that readers are well-informed about its implications for both accounting practices and investment decisions.

What is Goodwill on Financial Statements?

Goodwill on financial statements is classified as an intangible asset that reflects the premium a company pays over the fair value of the acquired business's identifiable assets and liabilities. It arises during a business acquisition when the price paid exceeds the net assets of the company acquired. Factors contributing to goodwill include:

- Brand reputation and customer loyalty

- Employee relationships and talent

- Market position and competitive advantage

- Intellectual property and proprietary technology

How is Goodwill Calculated?

The calculation of goodwill involves a straightforward formula that considers the purchase price of the acquired company and its net identifiable assets. The formula can be summarized as follows:

Goodwill = Purchase Price - Fair Value of Net Identifiable Assets

To illustrate this concept, let's consider a hypothetical scenario:

If Company A acquires Company B for $10 million, and the fair value of Company B's identifiable assets (assets minus liabilities) is $7 million, the goodwill would be:

Goodwill = $10 million - $7 million = $3 million

Why is Goodwill Important for Financial Statements?

Goodwill is crucial for several reasons:

- Reflects the premium paid for an acquired company, indicating confidence in future earnings.

- Affects a company's total asset valuation, influencing investment decisions.

- Impacts the financial ratios, such as return on assets and return on equity.

- Provides insights into management's acquisition strategy and growth prospects.

How is Goodwill Reported on Financial Statements?

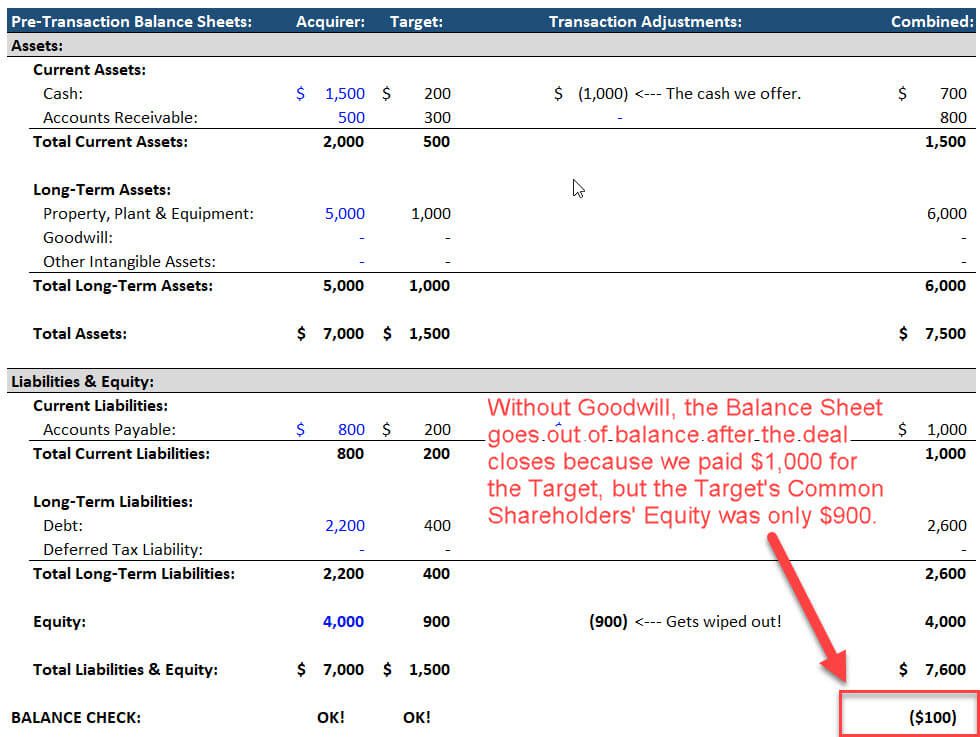

Goodwill appears on a company's balance sheet as a long-term asset. Unlike tangible assets, goodwill is not amortized but is subject to annual impairment testing. If the carrying amount of goodwill exceeds its fair value, an impairment loss must be recognized. This process involves evaluating the goodwill's recoverable amount, which can be complex, depending on various factors such as market conditions and business performance.

What are the Implications of Goodwill Impairment?

Goodwill impairment can have significant repercussions for a company's financial statements:

- Reduction in total assets, affecting the balance sheet and equity.

- Potential impact on earnings, as impairment losses are typically reported as expenses.

- Signal of declining business performance, which may affect investor confidence and stock prices.

How Does Goodwill Affect Investor Decisions?

Investors closely monitor goodwill on financial statements as it provides insights into a company's acquisition strategy and overall valuation. A high level of goodwill may indicate aggressive acquisition tactics, while frequent impairments could raise red flags about management's decision-making and the acquired business's performance.

What are the Challenges in Accounting for Goodwill?

Accounting for goodwill poses several challenges, including:

- Determining the fair value of acquired assets and liabilities accurately.

- Conducting annual impairment tests, which can be subjective.

- Maintaining transparency in reporting, as goodwill can obscure a company's true financial condition.

What Should Stakeholders Consider Regarding Goodwill?

Stakeholders should consider the following factors when assessing goodwill on financial statements:

- Evaluate the rationale behind acquisitions and the strategic fit of the acquired company.

- Monitor goodwill impairment trends and their impact on earnings.

- Understand the implications of goodwill on the company's overall valuation and market perception.

Conclusion: The Significance of Goodwill on Financial Statements

In conclusion, goodwill on financial statements is an essential concept that encapsulates the value of intangible assets acquired during business transactions. Understanding how goodwill is calculated, reported, and its implications on financial performance is crucial for investors, accountants, and business owners. By navigating the complexities of goodwill, stakeholders can make informed decisions and better assess a company's financial health and growth potential.