When it comes to accounting, understanding the intricacies of sales transactions is vital for every business. One of the common terms you might encounter is "n/30," which refers to the payment terms offered to customers. This term indicates that the net amount of the invoice is due within 30 days of the invoice date, providing a grace period for customers to settle their dues. Properly recording these transactions in the accounting journal is essential for maintaining accurate financial records and ensuring the smooth operation of a business.

In this article, we will explore how to complete the two necessary journal entries to record the sales transaction by utilizing the n/30 payment terms. Understanding these processes not only assists in achieving better financial management but also enhances your knowledge of accounting practices. Whether you're a business owner, accountant, or student, grasping these fundamental concepts can significantly impact your financial reporting.

The aim is to break down the complexities of recording sales transactions, especially under the n/30 terms. We will dive into the details of the journal entries and provide clear examples to illustrate these concepts. By the end of this article, you will not only understand how to record these transactions but also appreciate the importance of accurate bookkeeping in maintaining financial integrity.

What Are the Key Components of Sales Transactions?

Sales transactions typically consist of several key components that need to be recorded correctly. Here are some of the most significant elements:

- Invoice Number: A unique identifier for each sales transaction.

- Date of Sale: The date when the transaction occurs.

- Customer Information: Details about the customer making the purchase.

- Amount Sold: The total dollar amount of the sale.

- Payment Terms: The agreed terms for payment, such as "n/30."

How Do You Record Sales Transactions Using n/30 Terms?

Recording sales transactions under n/30 terms involves a systematic approach. You will need to create two journal entries: one for the sale and another for the receipt of payment. Here’s how it works:

What is the First Journal Entry for the Sale?

The first journal entry for recording a sale under n/30 terms involves recognizing the revenue and the accounts receivable. Here’s an example:

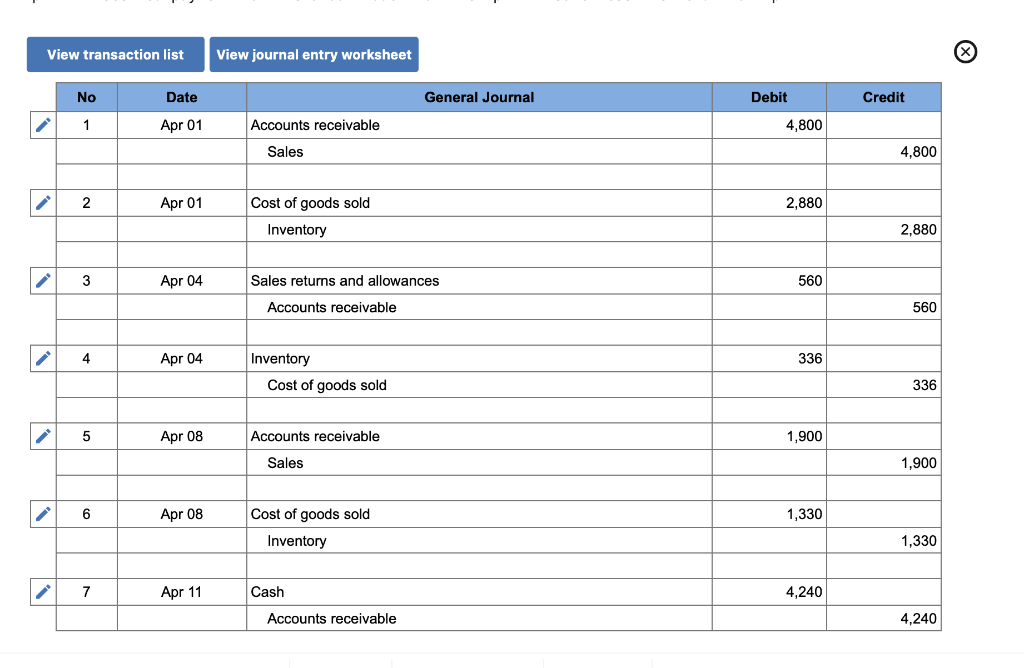

Date | Account Title | Debit | Credit ------------|-----------------------------|-------------|---------- YYYY-MM-DD | Accounts Receivable | $X,XXX | | Sales Revenue | | $X,XXX

What is the Second Journal Entry for Payment Receipt?

The second journal entry occurs when the customer pays the invoice within the 30-day period. This entry reflects the cash inflow and reduces accounts receivable:

Date | Account Title | Debit | Credit ------------|-----------------------------|-------------|---------- YYYY-MM-DD | Cash | $X,XXX | | Accounts Receivable | | $X,XXX

Why is Accurate Record Keeping Important?

Maintaining accurate records is crucial for several reasons:

- Ensures compliance with tax regulations.

- Aids in financial reporting and analysis.

- Helps in tracking customer payments and outstanding balances.

- Facilitates better cash flow management.

What Challenges Might You Face When Recording Sales Transactions?

While recording sales transactions seems straightforward, several challenges can arise:

- Data entry errors can lead to discrepancies.

- Misunderstanding payment terms can affect cash flow.

- Failure to follow up on outstanding invoices can result in bad debts.

How Can You Improve Your Accounting Practices?

Improving your accounting practices requires a proactive approach:

- Invest in accounting software to streamline processes.

- Regularly review and reconcile accounts.

- Stay updated on accounting standards and regulations.

- Implement a robust system for following up on receivables.

Who Should You Consult for Accounting Advice?

If you're unsure about your accounting practices, it's wise to consult a professional. Here’s who you might consider:

- Certified Public Accountant (CPA): Offers expert guidance on tax and compliance issues.

- Bookkeeper: Provides day-to-day financial record keeping.

- Financial Advisor: Helps with broader financial planning and strategy.

Conclusion: Mastering n/30 and Journal Entries

Understanding the n/30 payment terms and how to complete the two journal entries to record the sales transaction by is essential for effective financial management. By accurately recording sales and payments, businesses can maintain healthy cash flow, comply with regulations, and make informed financial decisions. Whether you are just starting or looking to refine your accounting processes, mastering these fundamentals will contribute significantly to your business's financial success.