In the world of accounting, documenting financial transactions accurately is crucial for businesses to maintain transparency and ensure compliance. One of the foundational aspects of this process is the ability to record the revenue part of the transaction and the second journal entry. This practice not only aids in tracking income but also plays a vital role in the overall financial health of an organization. Revenue recognition is a significant aspect of accounting, with specific guidelines governing how and when income should be recorded. By understanding how to record the revenue part of the transaction and the second journal entry, businesses can provide a clear picture of their financial standing to stakeholders, investors, and regulatory bodies.

Moreover, the effective management of these entries helps in preparing accurate financial statements, which are essential for decision-making. This article aims to delve into the intricacies of recording revenue and the corresponding journal entries, emphasizing key concepts and practical steps that businesses should follow. Whether you’re an accounting professional, a business owner, or someone interested in understanding financial processes, grasping these fundamentals is imperative.

As we navigate through this topic, we will explore various aspects of revenue recording, including its importance, the journal entry process, and common pitfalls to avoid. Join us as we uncover the essential elements of accounting practices that ensure businesses can effectively manage their revenue streams.

What is Revenue Recognition?

Revenue recognition is the accounting principle that determines the specific conditions under which revenue is recognized in the accounts. Understanding this concept is vital for accurately reporting financial performance. Revenue should be recognized when it is earned and realizable, regardless of when the cash is received.

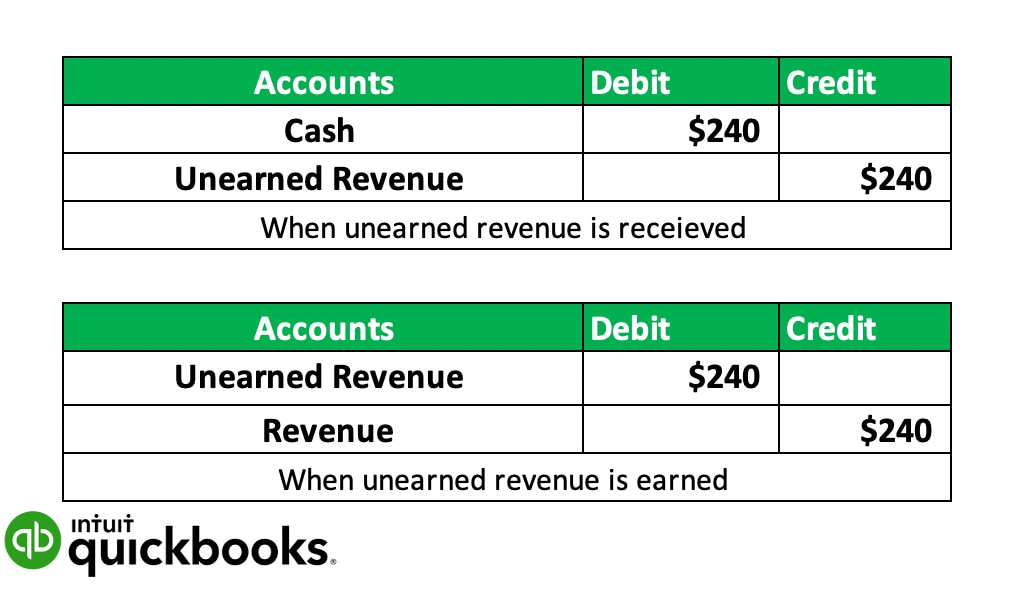

How to Record the Revenue Part of the Transaction?

To effectively record the revenue part of the transaction, businesses must follow a systematic approach that adheres to established accounting standards. Here are the steps involved:

- Identify the transaction and the parties involved.

- Determine the revenue amount to be recognized.

- Record the transaction in the appropriate journal.

- Ensure compliance with accounting principles, such as GAAP or IFRS.

What is the Second Journal Entry?

The second journal entry is crucial for accurately reflecting the financial implications of a transaction. It typically involves recognizing the corresponding expense or liability associated with the revenue recorded. This entry ensures that both sides of the transaction are balanced, maintaining the integrity of financial records.

How to Create the Second Journal Entry?

Creating the second journal entry involves the following steps:

- Identify the corresponding expense or liability related to the revenue.

- Determine the amount to be recorded in the second entry.

- Make the entry in the appropriate journal, ensuring it matches the revenue entry.

- Review both entries for accuracy and compliance.

What are Common Mistakes to Avoid When Recording Revenue?

When recording revenue and the second journal entry, businesses should be wary of several common mistakes:

- Failing to recognize revenue in the correct period.

- Inaccurate recording of amounts, leading to discrepancies in financial statements.

- Neglecting to consider the impact of discounts or returns on revenue.

- Not following established accounting principles and standards.

Why is Accurate Revenue Recording Important?

Accurate revenue recording is critical for several reasons:

- It ensures compliance with regulations and accounting standards.

- It provides a true representation of the business’s financial health.

- It aids in strategic decision-making and financial planning.

- It builds trust with stakeholders, including investors and customers.

How Can Businesses Improve Their Revenue Recording Processes?

To enhance the revenue recording process, businesses can implement the following strategies:

- Invest in accounting software that automates revenue recognition.

- Regularly train staff on accounting principles and practices.

- Conduct periodic audits to ensure compliance and accuracy.

- Establish clear policies and procedures for revenue recognition.

Conclusion: Mastering Revenue Recording and Journal Entries

In conclusion, understanding how to record the revenue part of the transaction and the second journal entry is essential for any business aiming for financial clarity and success. By following best practices and avoiding common pitfalls, organizations can ensure that their financial records accurately reflect their operations, contributing to informed decision-making and sustained growth. The journey to mastering these practices requires diligence, knowledge, and a commitment to accuracy, paving the way for a healthier financial future.